economic landscape.

In

addition to the sales volume

drought, average home prices are also exhibiting weaknesses.

In

Vancouver, widely considered Canada’s “bubbliest” city, average single

family home sale prices are down over 14% from their highs and average

condo prices are close to 2007 levels (

Brian

Ripley’s CHPC).

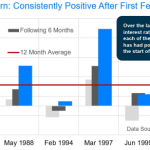

The

decade long shift in leadership between Canadian and US housing prices

is best observed through our charts on relative US/Canadian housing

markets (Section D–chart library).

Canadian markets of Vancouver, Toronto, and Montreal have now all

reversed bullish trends versus US markets which had been in place since

December of 2005 (See Vancouver Chart below). The only major

exception is Calgary, where home prices have continued their sideways

move relative to US home prices which began in

2009.

Chart

2)

Click Here to view a larger version of

this diagram

Leading

indicators of the economy

The

strength of the US and weakness of Canada is not confined to real

estate markets. Since our last update to the Canadian Real

Estate

Chartbook in December 2012, a pronounced shift in both Canadian and US

economies has taken place. The Canadian economy, once the envy of

Americans, Europeans, and others, is now widely viewed as a commodity

dependent, “one trick pony”.

Nothing better illustrates the economic differential than the OECD’s

leading economic indicators, which we first cited in our Winter 2013 newsletter

and are updated below. Canadian leading economic indicators

are

now falling behind US leading indicators by the widest margin in over

two decades.

Chart

3) – new

Click Here to view a larger version of

this diagram

Stock

markets, which are themselves a leading indicator of the future state

of the economy, have also diverged from one another. The Canadian

market and its foremost index, the S&P TSX composite, has

lagged

its US counterpart the, S&P 500, for the better part of two

years. In the interest of brevity we direct readers

interested in

a more detailed explanation of the divergence to our recently published

Spring 2013 newsletter.

Alternatively, the following chart is presented below illustrating the

extent of the recent Canadian underperformance. This ominous

pattern could foreseeably continue should drivers of the Canadian stock

market, notably global commodity demand, continue to weaken.

Chart

4) – new

Click Here to view a larger version of

this diagram

The

leading economic indicator which gives the most reason for pause is the

slowing new Canadian home starts, which are now declining on a

year-over-year basis and doing so at the fastest rate since the

financial crisis (see below). Bank of Montreal economist Sal

Guatieri recently addressed this fact by stating, “Canadian

home builders are facing the new reality that the decade-long housing

boom has ended” (Globe and Mail).

With 20% of Canadian GDP directly involved in construction and real

estate activities, a continued slowdown in housing-starts will have a

marked impact on the consumer behavior and ripple through other

consumer sensitive areas of the economy, including retail sales,

financial services, transportation, and warehousing.

Chart

5) – new

Click Here to view a larger version of

this diagram

Lacking

confidence

As

a consumer-driven asset class, real estate is intimately tied to

domestic consumer outlook. Due to this, it is important to note that

Canadian consumer confidence has slid stealthily lower since peaking in

early 2010. In fact, consumer confidence is now approaching

the

same levels last seen immediately following the financial crisis! (see

chart below).

Chart

6) – new

Adding

to the decline in consumer confidence are recent employment numbers

that indicate private Canadian companies, those most indicative of

overall economic health, shed 105,400 jobs in March and April

2013. This number of private sector job loss again mimics the

numbers last witnessed during the financial crisis.

The weakness in

the Canadian job market may come as a surprise to some readers as news

headlines

often indicate a reduction in the unemployment rate. The unemployment

rate has

been on a downward trend since the end of the recession, however, it

has stubbornly

failed to fall below 7%. This

is in

comparison to the sub 6% unemployment rates seen in Canada before the

recession.

In addition,

the overall unemployment rate does not always capture the true inherent

weakness in the employment environment due to the often misleading

inclusion of

individuals indicating their status as “self-employed”. Chief economist of Gluskin

Sheff, David

Rosenberg, recently commented on the significance of swelling US

self-employed

ranks by stating, the self-employed are, “…consultants

working out of their

basement offices and not exactly picking up much business…“

(Barrons). Thus the loss of private

sector jobs is a

critical weakness in the Canadian economy also voice by Benoit

Durocher, senior

economist of Desjardins Securities, “The

replacement of private-sector jobs

with independent work is usually not a sign of a healthy labour market.”

Globe and Mail

These findings

on unemployment are echoed in Canadian “Misery Index” (inflation +

unemployment rates), as illustrated below.

All major markets are signaling

upticks in misery. Toronto,

Montreal, and Vancouver are

exhibiting it above pre-recession lows, this despite barely-existent

inflation

and employment numbers that are likely understating reality.

Chart

7)

Click Here to view a larger version of

this diagram

Debt

burdens

We

reiterate our belief that the Canadian housing bull market of the last

decade has been primarily driven by credit expansion, a.k.a. increased

debt levels by Canadians. Readers are directed to Chart A2

in the chart library for support of this belief.

The desire for Canadians to take on more debt and thus more risk has

largely been due to low interest rates which now stand at a

generational low of less than 2% as indicated by 10 year government of

Canada bonds. These low rates have allowed for enhanced

cash-flow-affordability (not to be mistaken with actual affordability)

as home owners’ monthly mortgage interest expense has declined by –

over 11% since 2009. Notably, all other major components of

home

ownership costs including replacement costs, property taxes, insurance,

maintenance, furnishings, and miscellaneous expenses have grown at

least as must as Canadian core inflation and in some cases more than

twice as much! (See below)

Chart

8) – new

Click Here to view a larger version of

this diagram

How

large has the outstanding mortgage and consumer debt grown to?

Statistics Canada reported that in the final quarter of 2012 the

average Canadian household owed $164.97 in debt for every $100 of

disposable, after-tax income. In total, Canadian households now hold a

combined $1.1 trillion of mortgage debt and $477 billion of consumer

debt (Huffington Post).

To put this number into perspective, it is a large enough sum to

purchase every single publicly traded stock share listed on either the

Australian stock exchange (ASX), or the SIX Swiss Exchange, or even the

Deutsche Börse of Germany. The size of this debt relative to

the

entire Canadian economy (GDP) and its progression over time is

illustrated below. Canadian debt levels relative to GDP

appeared

to have now stalled near the 90% levels and the growth rate is far

below the heady days witnessed prior to 2010.

Chart

9)

Click Here to view a larger version of

this diagram

An

important finding that emerged recently is that Canadian debt burdens

are not largely borne by young first-time home owners desperate to get

into the housing market and thus overpaying and overleveraging

themselves. In fact, bankruptcy trustees Hoyes, Michalos

&

Associates were recently cited in a study finding that the highest debt

levels occur in the 50 to 59 year old age demographic. As one

trustee at the firm stated, “At a time

in their lives when they should be rapidly paying down debt, their

financial burden continues to grow.” (Canada Newswire)

This finding further identifies limitations on future credit expansion

and emphasizes the impact that demographic challenges will have on

Canadian real estate. Effectively, debt-burdened Canadians

approaching or entering retirement will be more reliant on wealth

currently locked in the form of home-equity. We touched on

the

role of Canadian demographics in real estate valuation in our last

chartbook (Chartbook Dec 2012)

Canadian

consumer debt burdens and the dependence on it by the domestic economy

and real

estate are best summarized by the Bank of Canada itself: “These

measures

[tightening government-insured mortgage lending standards] reduce

the

number one risk … to

the Canadian economy,“

– Former Governor of the

Bank of Canada Mark Carney, June 21 2012 Reuters

The

slowdown

The economic slowdown in Canada is difficult to ignore – the

International Monetary Fund (IMF) cut its growth outlook for Canada’s

economy to 1.5% from 1.8%, the weakest growth rate since the financial

crisis (Globe and Mail).

The Bank of Canada itself also cut domestic growth estimates in April

while indicating emergency-level low interest rates would persist (Maclean’s).

Despite low rates, the net result of such events is likely a headwind

for Canadian real estate markets. Sustained weakness in the

economy will only serve to burden Canadian consumers further.

In

addition, Canadian consumers have already extrapolated the persistence

of low interest rates further into the future than the Bank of

Canada. In other words, consumers have already reflected a

prolonged low rate environment into home price valuations.

Words

of the wise

A portion of our last commentary was dedicated to a summary of policy

errors that led up to the current state of excessive Canadian mortgage

debt. Recent tightening by the Finance Minister on lending

standards, although generally considered prudent, has been lobbied

against by those in the lending industry. The question now emerges:

Will Canadian Finance Minister, Jim Flaherty, reverse course on last

year’s mortgage tightening in the face of a weakening Canadian

economy? If his future actions are consistent with recent

statements made in Britain to the G7 finance ministers, then the answer

is “no”. Minister Flaherty was vocal in indicating that the

lack

of resolve by other G7 finance ministers to stick with debt reducing

austerity measures was an error. (Reuters)

At this

latest G7 meeting, not only did Minister Flaherty provide insight on

his

conviction to stick to austerity despite the economic hardships that it

creates,

he also shed light on how Canadian policy makers truly viewed the

Canadian

housing market prior to the latest round of tightening. “We are

seeing

moderation in the Canadian housing market. We did not have a bubble, but we

had the

beginnings of the indications of a bubble.”

– Jim Flaherty (Reuters). Readers are reminded that

any stronger

statement as to the existence of a bubble would be unlikely since it is

common practice

for policy makers to attempt to “talk down” fears.

Summary

We remain

bearish on the Canadian real estate market with real estate appearing

overvalued by approximately 30% in most major markets (See table). Canadian economic

weakness, the expected

contraction of outstanding consumer credit, and already heightened real

estate

prices serve as the basis for our bearish stance.

An update of

this chartbook will be made available in October/November 2013.

Real estate chartbook library

All charts not

referenced above are included below:

Due to changes with Google trends data, the housing bubble sentiment

grid has been discontinued.

Section A: Economics

Chart A1) Wages

vs. Home Price Growth

Chart A2) Canadian GDP, Home Prices, and Outstanding Mortgage Credit

Chart A3)

Population Growth and Housing Capacity

Chart A4) Consumer Credit Growth

Section B:

Valuation

Chart B1) Home

Prices over Present Value of Rents Chart

Table B1) Home Prices over Present Value of Rents Table

Chart B2) Home

Prices to Rents

Section C:

Real Index Values

Chart C1)

Canadian Real Rent Index

Chart C2) Canadian Real Home Price Index

Section D:

Canadian versus US Real

Estate

Chart D1) US Home

Prices vs Vancouver Home Prices –

Presented above in report Chart D3) US Home

Prices vs Toronto Home Prices Chart D4) US Home

Prices vs Montreal Home Prices

Chart D5) US Home

Prices vs Calgary Home Prices Section E:

City Summaries,

Home Price QoQ change, Inflation, Unemployment

Chart E1)

Vancouver

Chart E2) Edmonton

Chart E3) Calgary

Chart E4) Winnipeg

Chart E5) Toronto

Chart E6) Ottawa

Chart E7) Montreal

Chart E8) Halifax

Section F:

Home Price and Sales Pair

Volume Change for Major Canadian Cities

Chart F1) Canada

Chart F2) Vancouver

Chart F3) Calgary

Chart F4) Toronto

Chart F5) Ottawa

Chart F6) Montreal

Chart F7) Halifax

Section G:

Stocks vs Real Estate

Chart G1)

Canadian Stocks vs Canadian Real Estate (Long Term)

Chart G2) Canadian Stocks vs Canadian Real Estate (Medium Term)

Chart G3) US Stocks vs US Real Estate (Long Term)

Chart G4) US Stocks vs US Real Estate (Medium Term)

Section

A) Economics Return to Library

Chart

A1) Wages

vs. Home Price Growth

Canadian

wage growth versus home price appreciation from Feb 2003 to Mar 2013 is

reported below. Average weekly wage growth per home province

of

each city is reported. Also, only wages of full time workers

between the ages of 25 and 54 were examined in an attempt to capture

changes to the buying power potential of

first-time-homebuyers. In all ten markets examined, home

price

appreciation far surpassed average weekly wage growth.

Click Here to view a larger version of

this diagram Chart

A2) Canadian GDP, Home

Prices, and Outstanding Mortgage Credit

Appreciation

in Canadian home prices (from January 2000 onward) has more closely

reflected growth in mortgage credit rather than growth in Canadian

nominal GDP.

Click Here to view a larger version of

this diagram

Chart

A3) Population

Growth and Housing Capacity

In

all major Canadian housing markets housing capacity growth has exceeded

population increases between 2002 and March 2013. Calgary,

Edmonton, Ottawa, Montreal and Halifax are what we would consider to be

“severely overbuilt” with excess housing capacity of roughly 50% or

more than population growth over the same period. Vancouver,

Toronto, and Winnipeg, are “overbuilt” with excess housing capacity

close to 20% more than population growth over the examined

period.

Housing

capacity is defined as the number of individuals that can be reasonably

housed in new housing units, whether or not a new housing unit sits

unoccupied, under-occupied, or over-occupied. Assumptions

made

may be more appropriate for some markets over others.

Click Here to view a larger version of

this diagram

Chart

A4) Consumer

Credit Growth

Despite

falling interest rates, Canadian consumer credit growth has slowed to

the lowest levels in more than 12 years. This observation is

despite the fact that real bond yields, or inflation adjusted yields,

have dropped significantly. The axis on the right in

red

tracks 3 to 5 year real Canadian government bond yields which are now

below zero. In other words, interest income on these bonds

are no

longer sufficient to overcome lost purchasing power from the effects of

inflation. Should consumer and mortgage credit begin to

contract

then this will serve as a major headwind to future real estate

appreciation.

Click Here to view a larger version of

this diagram

Section

B) Valuation Return to Library

Chart B1) Home Prices

over Present Value of Rents

In

theory, residential real estate prices should equal the discounted sum

of future rental income. As a result, we have attempted to

estimate fair values for residential real estate in major cities by

comparing actual prices to theoretical discounted prices (valuation

ratio). In theory, this ratio should equal one and deviations

from this value should regress back to the value one over

time.

Note, discounted cash flow calculations are highly volatile and

dependent on underlying model assumptions. However based off

of

this methodology, Canadian real estate appears extremely expensive in

most major markets. Canadian real estate only appears

somewhat

reasonably priced if the assumption that current emergency low interest

rates continue indefinitely into the future. Any increase in

interest rates to even pre recession levels (which were also

historically low) causes Canadian real estate as a whole to appear

grossly overvalued.

Click Here to view a larger version of

this diagram Table B1) Home Prices

over Present Value of Rents

Using

the data from Chart B1 above, the following table attempts to quantify

the degree of price correction necessary to return the valuation ratio

in these five real estate markets back to the historical average

valuation ratio. The price corrections necessary to return

the

valuation ratio to the historical moving average range from -39% in

Montreal, to -31% in Edmonton.

Click Here to view a larger version of

this diagram Chart B3) Home

Prices to Rents

Canadian

home prices are currently not in line with historic multiples of

residential rental prices. Most extended from historical

norms

are Vancouver, Montreal, and Toronto. While Edmonton and

Calgary,

are elevated from historic averages but below previous witnessed

highs.

Click Here to view a larger version of

this diagram

Section

C) Real Index Values Return to Library

Chart

C1) Canadian

Real Rent Index

Canadian

residential rent increases have not historically kept pace with

inflation. While Canadian housing prices have surged higher,

renting has become relatively cheaper. This is evident from

the

chart below indicating long term trend of real-rents (inflation

adjusted) has been downward in most Canadian cities. This has

implications for retirees expecting to utilize rental income to finance

long term retirement expenditures. As with non inflation

indexed

bonds, cash flows from Canadian real estate may prove to be ineffective

to satisfy future increases in the cost of living. This is in

addition to the fact that residential real estate in Canada already

possess low rental yields, or the net annual rental income generated

from a property dividend by the current market value of the property.

Click Here

to view a larger version of

this diagram Chart

C2) Canadian

Real Home Price Index

Long

term real (inflation adjusted) annual home price returns have exceeded

3% in Vancouver and Victoria BC, while exceeding 1.5% in most other

large Canadian cities. Edmonton is the only exception with a

compounded annual house price appreciation of 0.64% over the examined

period. To put this into perspective, numerous examinations

of

long term real US home price appreciation indicate that they have only

slightly exceeded inflation at an approximate annual compounded rate of

0.5% per year.

Click Here to view a larger version of

this diagram

Section

D) Canadian versus US Real Estate

Return to Library

Chart

D2) US

Home Prices vs Toronto Home Prices

Click Here to view a larger version of

this diagram

Chart

D3) US

Home Prices vs Montreal Home Prices

Click Here to view a larger version of

this diagram

Chart

D4) US

Home Prices vs Calgary Home Prices

Click Here to view a larger version of

this diagram Section

E) Canadian City Summaries

Return to Library

The

following charts display a time series of unemployment, vacancy rates,

and quarterly home price changes for: Vancouver, Calgary, Edmonton,

Winnipeg, Ottawa, Toronto, Montreal, and Halifax.

Chart

E1) Vancouver

Click Here to view a larger version of

this diagram

Chart

E2) Edmonton

Click Here to view a larger version of

this diagram

Chart

E3) Calgary

Click Here to view a larger version of

this diagram

Chart

E4) Winnipeg

Click Here to view a larger version of

this diagram

Chart

E5) Toronto

Click Here to view a larger version of

this diagram

Chart

E6) Ottawa

Click Here to view a larger version of

this diagram

Chart

E7) Montreal

Click Here to view a larger version of

this diagram

Chart

E8) Halifax

Click Here to view a larger version of

this diagram

Section

F) Home Price and Sales Pair Volume Change for Major Canadian

Cities

Return to Library

The

following charts indicate annual changes in monthly home prices and

“sales pair” volume. Data has been generously made available

by Teranet – National Bank for: Canada, Vancouver, Calgary, Ottawa,

Toronto, Montreal, and Halifax. Please visit

http://www.housepriceindex.ca/ for the definitions and methodologies

used calculating their indices.

Chart

F1) Canada

Click Here to view a larger version of

this diagram

Chart

F2) Vancouver

Click Here to view a larger version of

this diagram

Chart

F3) Calgary

Click Here to view a larger version of

this diagram

Chart

F4) Toronto

Click Here to view a larger version of

this diagram

Chart

F5) Ottawa

Click Here to view a larger version of

this diagram

Chart

F6) Montreal

Click Here to view a larger version of

this diagram

Chart

F7) Halifax

Click Here to view a larger version of

this diagram

Section

G) Stocks versus Real Estate

Return to Library

Canadian

Real Estate versus Canadian Stocks (S&P TSX Index)

US

Real Estate versus US Stocks (S&P 500 Index)

Chart

G1) Canadian

Stocks vs. Canadian Real Estate (Long Term)

Displayed

in the chart below are Canadian home prices as a ratio of the TSX index

(Canadian stock market) from 1977. Seven cities are included:

Vancouver, Victoria, Calgary, Edmonton, Regina, Toronto, and

Montreal. Over the long term, home prices in Canada have

lagged price appreciation of stocks. Note, the stock index

below is a “price index” and therefore, excludes payment of dividends.

Click Here to view a larger version of

this diagram Chart

G2) Canadian

Stocks vs. Canadian Real Estate (Medium Term)

Displayed

in the chart below are Canadian home prices as a ratio of the TSX index

(Canadian stock market) from 1998. Nine cities are included:

Vancouver, Victoria, Calgary, Edmonton, Regina, Ottawa,

Toronto, Montrea, and Halifaxl.

Over the long term, home prices in Canada have lagged price

appreciation of stocks. Note, the stock index below is a

“price index”

and therefore, excludes payment of dividends.

Click Here to view a larger version of

this diagram

Chart

G3) US Stocks vs

US Real Estate (Long Term)

For

comparison purposes the following two charts (Chart G3 and Chart

G4) have also been included which display US home

prices as a multiple of the S&P 500 (US stock

market). The chart immediately below displays US home prices

as a ratio of the S&P 500 index (US stock market) from 1987

onward. Fourteen US cities are included in the chart below as

well as a composite index of ten major US Cities. Over the

medium term, home prices in Canada have outperformed price appreciation

of stocks. Note, the spike on the charts observed at March

2009 represent the stock market bottom during the financial crisis.

Click Here to view a larger version of

this diagram

Chart

G4) US Stocks vs

US Real Estate (Medium Term)

Click Here to view a larger version of

this diagram

Thank you to the following data providers:

{kind=link}