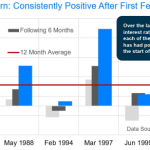

| 2013Q3 – Pacifica Newsletter – Taper Tantrum If the embedded document is not visible above, then the text and charts of the newsletter can be viewed below in html format: Investors Throw a “Taper” Tantrum Tapering Stimulus  The financial industry rarely has a challenge when coming up with clever headlines to describe the markets. Our newsletter gets its title from recent investor reaction to the mere hint that the US Federal Reserve (the ‘Fed’) may reduce or ‘taper’ its monthly $85 billion bond purchase program. Since bond prices and interest rates move in opposite directions, investors have taken great comfort in Fed bond purchases since they have provided fuel for financial markets while at the same time keeping interest rates anchored near generational lows. The reason that the Federal Reserve’s bond buying is so important to the markets can be seen by looking at how the Fed impacts the financial system. When the central bank buys bonds it is hoping that the sellers reinvest the proceeds of their bond sales into the financial markets. As these funds are channeled into these markets, the prices of financial assets such as stocks and bonds are expected to rise which will then create a “wealth effect”. The “wealth effect”, according to economists, is the idea that when individuals feel wealthier due to an increase in the value of their assets they will spend more. Thus, the Federal Reserve is wagering on the idea that rising asset prices would help higher spending to take root. This would in theory lead to a boost in economic output and eventually jobs. That is the theoretical concept and to be fair, the low interest rate environment which the Fed has helped to create has helped the recovery in US real estate. In addition, the US auto industry has powered up and automobile production has rebounded strongly. These vital segments of the US economy are especially important because they are able to generate so many spinoff jobs. Stimulus Addiction As of the first quarter of 2013, the world’s central banks had injected over $12 trillion of stimulus into their respective economies since the start of the global financial crisis. This is in addition to cutting interest rates to near generational lows. Markets have now become accustomed, if not reliant, on accommodative monetary policy. This reliance became apparent through investors’ reaction to even the hint of stimulus tapering. On May 22 nd , the head of the US Federal Reserve, Ben Bernanke, told Congress that the central bank might wind down its monetary easing stance. The response: equities around the world sold off and interest rates rose quickly.

Chart source: FactSet Of course, this reaction was not contained to the US. Interest rates were impacted throughout the world. In North America, mortgage rates have moved up quickly and some observers say it is already impacting US real estate sales. As the chart above shows, the “taper tantrum” caused the US 30 year mortgage rate to rise by 1.15% in a two month period and mortgage refinancing activity simultaneously fell by more than 50%. Offsetting this interest rate spike is the fact that home affordability in the US remains comfortably above historic levels.The reaction from the markets was so quick and strong that the Federal Reserve attempted to walk back the earlier comments and go out of its way to clarify what Bernanke meant to say. It should be noted that the minutes from recent Fed meetings reveal that Bernanke was not alone and had support from other Fed governors to begin trimming monetary stimulus if necessary. What Bernanke actually said according to the transcripts from the Federal Reserve is that the improving labor markets and the expected gradual rise in inflation towards its targeted two percent rate would dictate further policy actions such that, “… if the subsequent data remain broadly aligned with our current expectations…,we would continue to reduce the pace of purchases in measured steps through the first half of next year.” If that were not enough to make the markets to perhaps rethink their reaction, Bernanke also stated that he wanted to “… emphasize once more the point that our policy is in no way predetermined and will depend on the incoming data and the evolution of the outlook.” In short, the Fed will look at the data and decide the appropriate course of action in the future. Perhaps the most important variable in determining Fed policy will be US jobs data. Even the traditional main focus of inflation will likely play second fiddle to the unemployment rate. As the chart below shows, the US economy has been able to add over 7 million jobs over the last 40 months. Although this might sound impressive at first, the job additions work out to less than 200,000 jobs per month. To put this into perspective, the US economy needs to generate about 350,000 jobs per month to keep up with the growth of the labor force and to keep the unemployment rate on a downward trend.

Chart source: Market Watch, US Department of Labor Also disguised in recent US labor data is the sobering fact that the number of US workers with part-time jobs who have indicated that they would prefer a full-time position if possible sits at 8.2 million – the highest in eight months. In comparison, 11.8 million Americans are “unemployed”. It bears clarifying that the official unemployment rate oes not take into account individuals who have simply given up looking for work or are unable to search for work for various reasons. These individuals total an additional 2.6 million. Although the unemployment data is humbling to policy makers, on a positive note, wages have begun to turn up and the average work week has also been improving since the recession ended. Policy Limits On the one hand markets are dreading the day the Fed eases back on its stimulus, yet on the other, the Fed’s policies have not been effective for the millions of people looking for full time employment. The job creation gap is putting a spotlight on the limits of monetary policy. Equally frustrating for the Federal Reserve is that despite injecting trillions of dollars of capital into the US banking system the lack of credit creation from banks has been lacklustre. Simply put, banks aren’t lending enough and households and businesses are reluctant to take on debt. In some ways this amounts to a failure by businesses and consumers to take sufficient advantage of the Fed’s current generosity. Growth in bank lending is a vital element for the Fed’s efforts to succeed. Ultimately, every bond purchase by the Fed ends up increasing the bond seller’s bank reserves. Reserves are the amount that a bank can lend out. Historically, as excess reserves were lent out by the US banking system, each dollar of reserves created by the Federal Reserve amounted to about a $70 increase in the money supply. However, after the financial crisis, this has dropped to only a meager $1.50 increase in the money supply. A rising money supply acts as a source of energy for the economy. The excess reserves that are not being borrowed by consumers and businesses (lent by banks) is now approaching a staggering $2 trillion.

Goldilocks Growth

Financial markets may be able to handle a stimulus exit if the global economy can continue to grow at a goldilocks pace of ‘’not too hot and not too cold’’. In such a scenario, bond markets will be relieved that the pace of tapering will be gradual. Meanwhile equity markets may hope to offset the gradual drag of higher borrowing costs through a slow and steady rise in corporate earnings. Unfortunately, second quarter 2013 reported earnings are not too spectacular. Sales growth is coming in at the lighter end of expectations and companies are indicating global challenges remain. These challenges arise from Europe continuing their austerity and debt struggles, China and India showing slowing economic growth and Brazil – the engine of Latin America — floundering with a bout of rising inflation and slowing economic growth. Brazil’s economic challenges can be highlighted by the fact that the consensus forecast for Brazil’s economy calls for a 2.3% growth rate while inflation has increased to 9.4%. Currently, Brazil’s economy is achieving the lowest economic growth rate in 24 years. To be sure, much of the front page exuberance about Brazil has faded.

US Leads the Way Forward

Fortunately, Europe seems to have passed the worst of its decline and the European Central Bank’s pledge to “do whatever it takes” seems to have gotten the markets’ collective attention. In addition, the worst of the government spending cuts across Europe seems to have passed – allowing the economy a chance to stabilize. The latest data show that manufacturing is beginning to rebound and the economy is no longer contracting. Europe’s plight can at this point be best summarized as “a little growth is better than no growth’’. The continent’s economy is being led by the German manufacturing sector. Surprising to some might be the fact that Chinese manufacturing data is continuing to show weakness under the dual pressures of slowing export growth and relatively tight monetary policy in China. The Chinese government is taking the hard road in order to correct some of the imbalances in its economy. These imbalances have been brought about by years of excessive investment that has created a massive oversupply in everything from housing to roads to industrial capacity. The slowing Chinese economy and the government’s clamp down on construction has impacted the global demand of commodities such as copper and steel.  Even in the face of reduced Chinese commodity demand, Canada may surprise economists to the upside. With roughly 75% of Canadian exports heading to the US, strength in the US economy may serve to offset other growth anchors. The firming of oil prices has also been a boon to the critical Canadian energy sector which has faced challenges due to constrained distribution channels as we noted in our last newsletter. If recent retail sales numbers in

Canada are any indication of what is in store for the Canadian economy then the Bank of Canada’s projections for the Canadian economy will likely be revised upward for 2013 with retail sales rising 1.9% in May vs. an expected 0.3% consensus gain amongst economists.Clearly, markets are watching the economic data around the world. In particular, US data is being filtered through the lens of whether or not it will lead to higher interest rates. In Europe the focus is whether or not the data can continue to confirm that the European economy has escaped its long recession. For China, the markets will likely want to see continued stabilization of the economy and a sign that tighter lending is bringing property prices down to a sustainable level. The big three economic blocks of Europe, China, and the US will decide which way the economic recovery goes from here.

Pacifica Partners Capital Management Inc.

This report is for information purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. The information contained in this report has been compiled from sources we believe to be reliable, however, we make no guarantee, representation or warranty, expressed or implied, as to such information’s accuracy or completeness. All opinions and estimates contained in this report, whether or not our own, are based on assumptions we believe to be reasonable as of the date of the report and are subject to change without notice. Past performance is not indicative of future performance. Please note that, as at the date of this report, our firm may hold positions in some of the companies mentioned.

Social Media: It is Pacifica Partners Capital Management Inc.’s policy not to respond via online and social media outlets to questions or comments directed to it or in response to its online and social media publications. Pacifica Partners Capital Management Inc. does not acknowledge or encourage testimonials posted by third party individuals. Third party users that have bookmarked Pacifica Partners Capital Management Inc.’s social media publications or profile through options including “like”, “follow”, or similar bookmarking variations are not and should not be viewed as endorsement of Pacifica Partners Capital Management Inc., its services, or future or past investment performance. To view our full disclaimer please click here.Copyright (C) 2013 Pacifica Partners Capital Management Inc. All rights reserved. |

|

|

|