If

the embedded document is not visible above, then the text and

charts of the newsletter can be viewed below in html format:

Canada & the USA, a Tale

of Two Economies

Canada

Out-of-Step With the US

When

two countries are as interconnected as Canada and the US, it is often

the case that their respective economic circumstances are at least

somewhat similar. For these two North American neighbors, however,

their economies and stock markets have diverged considerably over

recent months. This shouldn’t come as too much of a surprise, as we had

indicated in our last newsletter that leading economic indicators of

each economy were already signaling a slow down in Canada’s economy and

a much awaited resurgence of the US.

It

is important to point out that stock markets are only a partial

reflection of the overall economy. And despite ebbs between the

performance of Canadian and US economies, historically their two stock

markets have been highly correlated. More recently, however,

a pronounced divergence has emerged with Canadian stock markets

remaining relatively flat over the last year as US stocks marched

higher. This disconnect is illustrated below.

If

one were to search for an explanation for this divergence then the

fundamentals of the Canadian economy and slowing global commodity

prices are a great place to start. One of the biggest reasons for this

underperformance has to do with the makeup of the two countries’

markets. Approximately 40% of the Canadian stock market is made up of

natural resource stocks – more than double the 15% resource exposure of

the S&P 500 (US Stocks).

Canada’s Decade

of Success

For

much of the last decade, rising commodity prices were a strong tailwind

to Canadian equities. The world was knocking on Canada’s door. The

allure of the riches of the Canadian oil sands, robust commodity

consumption from China and an appreciating Canadian dollar made

Canadian equities attractive assets. As this went on, the capital

inflows into Canada from around the world made Canadian equities even

more attractive.

The Energy

Sector

The Canadian energy sector, which comprises over 25% of the

S&P/TSX index, has in large part acted as an anchor on Canadian

equities.

While the price of oil has stayed relatively high, Canadian oil

companies have not been able to benefit as much as their US

counterparts. In fact, for much of 2012, Canadian oil companies were

receiving up to $20/barrel less for oil shipped to the US. This was due

to limited US refinery capacity, pipeline constraints, and rising US

oil production that combined to create a glut of oil.

Profits for the Canadian energy sector declined by more than 50% in

2012, to a little more than $7 billion which is on par with 1999

levels. As the sixth largest oil producing nation in the

world, the discount that Canadian oil companies receive on their crude

production has an economic impact. Estimates indicate losses

due to the discount in pricing to be upwards of $15 billion to $18

billion per year.

This issue will likely continue to confront our oil producers for some

time as pipeline capacity will continue to be constrained even if the

Keystone XL pipeline wins approval later this year from the Obama

Administration. The 830,000 barrel/day pipeline would not start moving

oil until late 2014 at the earliest. The chart below illustrates its

proposed route from Hardisty Alberta to Cushing Oklahoma.

Chart

source: Canadian Association of Petroleum Producers (

www.capp.ca)

As investor confidence has been jarred by the developments in the

Canadian oil sector, it has left many of the largest oil producers in

Canada trading at very cheap valuations – rivalling the levels reached

during the recession. These valuations plus their strong

track records of dividend growth has made them very attractive

investments. After releasing first quarter 2013 earnings, Canadian

energy giants, Suncor and Canadian Natural Resources raised their

dividends by 54% and 21% respectively.

The catalyst to unlock this value and move stock prices higher will

come from the approval of new pipelines that will move Canadian crude

faster to the US Gulf Coast, Eastern Canada and to the Pacific Coast

where Canadian oil companies will be able to access Asian markets. The

access to Asia is especially important as US energy production

continues to rise and China assumes its expected title of world’s

largest oil importer. According to the International Energy Agency, US

production of oil will help to lower US oil imports from 10 million

barrels/day in 2010 to about six million/day by 2035. As of the end of

April 2013, US oil production stands at 7.3 million barrels/day which

is up nearly 20% from a year ago.

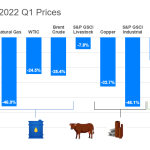

Commodities

Sector

Another drag on the Canadian stock market has been the sharp drop in

agricultural and base metal prices. Commodity stocks represent almost

20% of the Canadian stock market while they are less than 1% of the US

S&P 500.

Copper has earned the nickname of “Dr. Copper” for its reputed ability

to call turning points in the economy. Oftentimes, copper prices have

turned higher or lower in anticipation of the economy’s turning points.

Copper prices have fallen by about 5% over the last two years. A large

part of the reason for the decline in copper prices is likely due to

fears about the Chinese economy.

China’s leadership has made a central plank of its policies the

intention to make the Chinese economy less reliant on construction and

capital investment. The excessive reliance on construction and capital

investment has led to fears of a bubble in property and overinvestment

in various industrial sectors. In addition, the European Union is the

second largest consumer of copper and it is mired in recession which

has hindered copper demand further. Offsetting this weakness

is the budding rebound in US construction.

Financial Sector

When

the Great Recession ended in 2009, Canadian banks were trading at a

significant premium to banks in most countries. Gradually, the rise in

the stock prices of US banks has helped to narrow the valuation gap

between Canadian and US banks. In recent quarters, investor fears about

Canadian consumer debt and elevated house prices have made investors

cautious on Canada’s banks. The fear arises from the distinct

possibility that a decline in Canadian real estate will impact banks

through rising mortgage defaults and a made-in-Canada debt-reduction

process.

North American

Economic Landscape

When the Great Recession ended in 2009, one of the most repeated

predictions was that the US savings rate would rise to match the levels

of the 1960s and 1970s. The thought was that consumers had undergone a

generational change in mindset towards spending and saving as a result

of the economic turmoil that had enveloped the global

economy. After a brief rise in the immediate aftermath of the

Great Recession, the personal savings rate in the US has fallen once

again to 2.3%. While this has helped the US economy achieve one of the

best economic growth records amongst the advanced economies, the low

savings rate is a function of poor wage growth. In fact, wages as a

percent of the US economy are at a record low.

Stagnant wage growth has helped to propel US corporate profits and they

are now at a record level as a percentage of the US economy. As Ron

Perelman, the chairman and CEO of Revlon stated recently in an

interview:

“Unfortunately

what is good news for American industry…is bad news for those looking

for work …We’ve rationalized our businesses over the last five years…

those people that we laid off in 2008-2009, there’s no need for us to

hire back … We’ve gotten more efficient and we’ve gotten more

productive.”

– CEO of Revlon

As the current economic recovery has been sub-par by historical

standards, corporations have struggled to maintain revenue growth so

they have been focusing on cost controls to help meet profit

expectations. Corporate profit growth in the US was lower in 2012 than

2011 but the US market has been able to overcome slowing profits

because investors have given the economy the benefit of the doubt. The

Price-to-Earnings (P/E) ratio has risen to about 16 – meaning investors

are willing to pay $16 for each dollar of corporate profits.

This has allowed the market to continue higher as central banks around

the world are going to remain ultra-accommodative and help to ensure

liquidity is well supplied to the markets. Though economic data has

been disappointing in recent weeks, investor confidence is strong and

the demand for equities has been resilient.