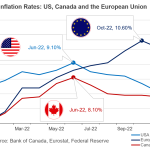

As

interest rates in the US have risen, the weakness of emerging markets

nations has been exposed. Chief amongst them is the fact that they have

been borrowing and spending more than they ought to have while their

imports have been rising too quickly. The imports are being fuelled by

easy money policies that are aimed at continuing the economic recovery.

As the US makes a switch towards a slightly less accommodative monetary

policy and its interest rates rise, international capital flows have

been coming to the US – leaving the US dollar stronger and the

currencies of the emerging markets nations weaker (see chart below).

Click here to view a larger

version of this chart.

These nations cannot afford a weaker currency because it tends to fuel

inflation in their economies by making their imports stronger. The only

cure for inflation and the discouraging of the capital exodus is to

raise interest rates. But here is where it gets challenging for them:

if they raise interest rates, their economic growth rates will weaken

and capital outflows will only increase once again. So begins a vicious

circle as selling begets more selling. Some emerging markets countries

have tried to shock their currencies higher by raising interest rates

by 3-5% in one fell swoop. So far, markets have calmed down but the

consensus is that this is not enough as investors believe that

ultimately these countries will have to walk away from higher interest

rate policies. They believe that they will buckle under the pressure of

trying to maintain economic growth rather than price or currency

stability.

A textbook illustration of this scenario is playing out in India. A

falling currency and rising inflation have left India’s central bank

between a rock and a hard place as it must choose between stopping

inflation with even more vigor (raising interest rates again) and

holding economic growth back still more. India’s central bank has gone

so far as to call for central bank decision making to be more

coordinated globally. While this is easier said than done and perhaps

not even feasible given that the economic constraints of nations vary

so widely, it is a recognition that the US footprint is cast far and

wide and ultimately the decisions of the US central bank have

implications for the international community. The Fed has been

unusually blunt in responding to critics who blame US monetary

tightening for the problems of the emerging economies. Jeffrey Lacker,

a Federal Reserve governor was recently quoted as saying that its

policies are conducted strictly towards its mandate of “price stability

and maximum employment here in the United States.”

China is also suffering from the after effects of its ultra-easy

monetary policies that was implemented to combat the effects of the

financial crisis in 2008. China’s monetary stimulus far exceeded the

one undertaken by the US even though its economy was less than half the

size of the US economy. Chinese policy makers have come to grips with

the fact that they have lost control of their economic levers and have

begun to crack down with vigor on lending activity within the Chinese

economy. Several times in the last three months, Chinese banks have

found a severe lack of liquidity and overnight interest rates ended up

spiking to nearly 9 percent as the Chinese central bank sought to send

a message to the banking industry that it was serious in its attempts

to cool lending activity.

One of the great debates in the financial markets is whether or not

China will suffer a hard landing or a gentle slowdown. As we have

highlighted in past commentaries, China’s problems are rooted in too

much lending that is fueling an excess in the construction of housing

and factory capacity. According to data from the International Monetary

Fund, China is only using about 60% of its industrial capacity even

though the economy is growing at over 7 percent annually according to

the latest government data. The challenge of Chinese policy makers is

to ensure that they are able to engineer a slowdown that does not turn

into something more severe.