Pacifica Partners 2013

Winter Newsletter – Debt, Profits, Canada & more

>If the

embedded document above is not

visible, the text and charts have also been included below as follows:

Turning the Page on the Fiscal Cliff

In

the final hours of the 2012 trading year, the financial markets showed

their relief that Congress and the White House had reached an agreement

and the “Fiscal Cliff” would be averted. The collective attention of

the markets is now turning to the Debt Ceiling talks which involve

Congress signing off on yet another increase in the borrowing limits of

the US. Given that the US debt limit has been raised at

regular intervals, some Congressional members are not willing to rubber

stamp yet another debt limit increase. This sets the table

for the next potential fight between Congress and the President and is

one that could upset investor portfolios. Essentially, the

“national credit card” of the US could be maxed out against the debt

ceiling. Without an agreement that would allow the US to borrow more,

the US could begin to default on its $16.4 trillion debt. The markets

would not take kindly to such an event.

Fortunately,

this is not a high probability event – though it could

still provide the markets a bumpy ride. Currently, the markets are

pricing in a scenario of yet another 11th hour deal.

Investors here find themselves at polar opposites. The pessimistic side

believes that the national debt is too high a hurdle for the economy to

overcome and the deleveraging process will continue for some time yet.

The bullish argument is that the economy is on the mend with a

rebounding housing and auto sector leading the way. Add in low

inflation, a Federal Reserve willing to hold interest rates lower for

longer, and rising corporate earnings and we have an attractive

environment. Globally, central banks are continuing their bold efforts

to seemingly do whatever it takes to ensure their respective economies

are strengthened. Nearly 40 central banks around the world are engaged

in aggressive monetary easing in order to stimulate their economies.

Putting Money to Work

Investors

have been so cheered by this backdrop that for the week ending January

9th, they have put more capital to work into equity mutual funds in the

US than any other single week since October 2007. A similar occurrence

took place when US markets were peaking before the financial crisis.

This is a marked turnaround from the trend that has prevailed for the

last five years as investors withdrew close to $500 billion from US

equity mutual funds while adding $1.2 trillion to bond funds according

to the Investment Company Institute (see chart above).

This trend has also caught on in emerging markets (China, India,

Brazil, Russia, etc.). According to Morgan Stanley, emerging market

stock funds have seen cash inflows for 18 consecutive weeks. In

comparison the previous record was 29 weeks of money inflows ending

December 2010.

As we have highlighted over the years, such data points are not

comforting. In fact, extremes in investor fund flows tend to be a

contrarian indicator as mutual fund investors often invest by piling

into fads or assets that have already been bid up. It should be noted

that the last time we observed this much of an increase in investor

risk appetite, US equities tumbled 57 percent in almost 18 months after

the S&P 500 stock market index reached its peak in October

2007. However, no one indicator can be used in isolation and

there is currently a modest undercurrent of strength to the global

economy.

Any Deal is Better than No Deal Officially called the American Taxpayer Relief Act of 2012, the fiscal

cliff deal will raise revenue of $617 billion over the next ten years

as compared to the option of allowing the Bush tax cuts to carry on.

Over $540 billion will come from households making over $1 million per

year. While the budget deal provides markets with temporary relief from

anxiety, critics believe that the tax impact will actually raise taxes

on almost 80% of US taxpayers through higher income taxes, payroll

taxes or both. They state that the impact of the higher taxes will hurt

the economy while the US federal deficit will likely remain in the

frightening $1 trillion range and the debt-to-GDP ratio for 2013 will

still climb to about 107% of GDP from the current 100% level. The

budgetary challenge for the US will lie in whether or not the increase

in tax revenues outweighs the drag on the economy that those same tax

increases will create. Looking at the US budgetary numbers, this much

is clear: the budget will continue to be a headwind until the

tough

decisions on spending controls on entitlement programs and defense

budgets are made.

Canada is going to be impacted by whatever route the US economy takes.

Domestic challenges to the Canadian economy are only now starting to

make the front pages. For some time, our commentaries and newsletters

have tried to make the point that Canadian consumer debt, elevated

house prices and accelerating government spending at the federal,

provincial and municipal levels could combine to hinder future economic

growth.

The Bank of Canada has kicked off 2013 with some candid comments

suggesting the economy is going to take longer to recover and rates

will stay low for sometime. One of the objectives of the fiscal and

monetary authorities in Canada has been to slow the increase in

household credit. To this end, the data are moving in the

right direction as the increase in household credit has been moderating

from a 5.5% growth rate to a little more than 3% in the most recent

quarter. This is the lowest rate of growth since 1999 and is being led

by slowing mortgage credit. However, the troubling fact is that this

slower increase in credit is still above the growth of disposable

income which means that consumer debt is still rising faster than

incomes.

Amazingly, in a few short years Canadian consumers have managed to

increase their debt levels to beyond the levels that US consumers had

at the beginning of the collapse in the US real estate market. The

latest data from the Bank of Canada shows that the ratio of household

debt to income is at 165%.

Therein lies the challenge for Canada’s economy. Canadian consumer

spending accounts for 58% of GDP but debt levels are already at record

highs. Thus, consumer spending will not be able to lead in any

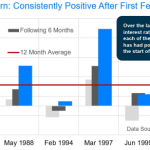

significant way a potential rebound in economic growth. As the chart

above shows, Canada’s leading economic indicators point to a Canadian

economy that will lag the United States and the rest of the G7.

While Canadians have been accustomed to tax cuts over the last fifteen

years, it is highly unlikely that Canadian taxes will be able to fall

any further. The deterioration in the budgetary picture at all levels

of government will likely mean higher taxes – further restraining the

economy and disposable income.

Profits and Expectations

For several quarters, most analysts have been lowering their

expectations for profit growth. This is due to the fact that GDP

numbers for much of the world are coming in lower than expected.

However, as the bar has been lowered successively, most companies have

been able to jump over the bar to the relief of investors. The bearish

argument around corporate earnings is that earnings growth has slowed

and revenue growth has all but stalled. According to data from Thompson

Reuters, current expectations are for US corporate earnings

to rise 1.9% year over year. Three months ago, expectations were for a

9.9% annual increase and six months ago it was for a 13.7% increase.

Clearly, expectations have come down.

This

is significant because revenue growth is tied to growth of the economy

(GDP growth). If GDP growth rates stall or come in under

expectations, corporate revenue is likely to come in under

expectations. Therefore, corporations would not be able to

meet the expectations that are built into stock prices. Thus far,

fourth quarter 2012 earnings announcements are beating expectations by

more than 2 to 1 – albeit on lowered expectations.

Currently, the S&P 500 is trading at a level of approximately

13.2 times 2013 earnings estimates which makes the market cheaper than

the longer term average of closer to 15 times. While the US stock

market is not cheap, it is fairly valued. In order for the

market to continue to be fairly valued, global GDP will have to

continue to strengthen and corporate profit margins must hold steady.

As a percentage of US GDP, corporate profit margins in the US are at

record highs as wages have been restrained, interest rates are low and

corporate balance sheets are pristine.

These characteristics have allowed S&P 500 corporations to buy

back over 8 billion shares (net) over the last twenty-one months,

thereby providing support to stock prices. As of 3Q 2012, the

S&P 500 companies had about 300 billion shares outstanding –

which was the lowest number of shares since mid 2009.

While the markets have somewhat elevated expectations, an improving

economy and a calmer macro- economic environment will help to support

the markets. The key outcome to monitor will be to see whether revenue

growth, corporate profit margins, and earnings continue to make stocks

an attractive asset class.

Pacifica

Partners – Capital Management

Navigating

a Sea of Opportunity

This

report is for information purposes only and is neither a solicitation

for the purchase of securities nor an offer of securities. The

information contained in this report has been compiled from sources we

believe to be reliable, however, we make no guarantee, representation

or warranty, expressed or implied, as to such information’s accuracy or

completeness. All opinions and estimates contained in this report,

whether or not our own, are based on assumptions we believe to be

reasonable as of the date of the report and are subject to change

without notice. Past performance is not indicative of future

performance. Please note that, as at the date of this report, our firm

may hold positions in some of the companies mentioned. Social

Media: It is Pacifica Partners Inc.’s policy not to respond via online

and social media outlets to questions or comments directed to it or in

response to its online and social media

publications. Pacifica Partners does not

acknowledge or encourage testimonials posted by third party

individuals. Third party users that have bookmarked Pacifica

Partners’ social media publications or profile through options

including “like”, “follow”, or similar bookmarking variations are not

and should not be viewed as endorsement of Pacifica Partners Inc., its

services, or future or past investment performance. To view our full

disclaimer please click

here.

Copyright

(C) 2013 Pacifica Partners Inc. All rights reserved.